Coca-Cola vs. PepsiCo: Who Will Reign Supreme?

The Global Beverage Rivalry: Coca-Cola vs. PepsiCo

In the global beverage industry, few rivalries are as iconic as the one between The Coca-Cola Company and PepsiCo, Inc. These two giants dominate the market, commanding a significant share of the soft drink industry while expanding into various categories such as snacks, juices, energy drinks, and bottled water. Their ongoing competition shapes consumer preferences and redefines the concept of refreshment, with each company employing distinct strategies to maintain their leadership.

The Case for Coca-Cola (KO)

Coca-Cola's investment case is built on its enduring market dominance, strategic agility, and global reach. The company holds one of the largest shares in the non-alcoholic ready-to-drink market and has achieved 18 consecutive quarters of value share gains. Its extensive beverage portfolio includes sparkling soft drinks, juices, dairy, hydration, and energy categories, allowing it to remain relevant across different demographics and income levels.

North America continues to be a key driver of performance, with sequential volume improvements. Meanwhile, fast-growing regions like India, Brazil, and Africa contribute to long-term growth through affordability-led expansion and localized innovation. Coca-Cola’s business model blends brand strength with operational efficiency, supported by a digital-first marketing transformation that deepens consumer engagement through personalized campaigns.

The company’s refranchising efforts in regions like India and Africa have sharpened its focus on core competencies, driving operating margin expansion and freeing capital for innovation. Coca-Cola’s portfolio balances affordability and premiumization, with offerings like mini-cans, smartwater, Topo Chico, and fairlife catering to evolving lifestyles and health-conscious consumers.

Despite challenges such as tariff and trade frictions, including Mexico’s sugar tax, Coca-Cola remains well-equipped to sustain profitable growth and long-term value creation. The company delivered 6% organic revenue growth in the third quarter of 2025, with margin expansion despite currency and cost headwinds. Strong free cash flow generation, projected near $10 billion, supports continued reinvestment and shareholder returns.

The Case for PepsiCo (PEP)

PepsiCo remains a global powerhouse with a balanced and diversified model spanning beverages and convenient foods. Its beverage arm, led by brands like Pepsi, Mountain Dew, and Gatorade, continues to expand across categories, including energy, functional hydration, and modern sodas like poppi. Meanwhile, its food segment, anchored by Frito-Lay, Quaker, and Sun Chips, contributes roughly half of overall revenues, making PepsiCo unique in the consumer staples universe.

The company’s international business accounts for about 40% of total net revenues, delivering consistent mid-single-digit growth. PepsiCo’s growth engine is powered by relentless innovation and digital acceleration, with a focus on portfolio reshaping, automation, and AI-led efficiency. Its efforts to cater to affordability and premiumization trends include a leaner SKU base and optimized price-pack architecture.

In beverages, PepsiCo focuses on functional and health-oriented innovations, such as Pepsi Prebiotic, Gatorade Lower Sugar, and Propel Protein Water, to expand its reach among wellness-conscious consumers. The company’s global snacks revamp, featuring offerings like Lay’s and Doritos NKD (no artificial colors or flavors), underscores its commitment to transparency and nutrition.

PepsiCo delivered nearly 3% reported net revenue growth in the third quarter of 2025, marking its 18th consecutive quarter of resilient international momentum. Despite EPS headwinds from tariffs and global input costs, the company’s cost-reduction programs and digital productivity initiatives are offsetting inflationary pressures. As PepsiCo modernizes operations and sharpens execution, it positions itself as an agile, innovation-driven leader.

Price Performance & Valuation

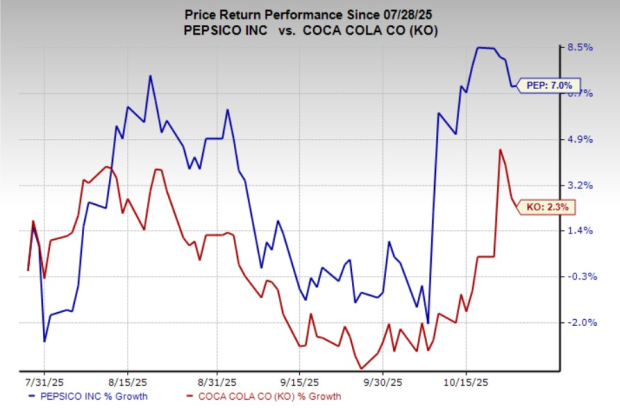

Shares of PepsiCo have seen a 7% increase over the past three months, driven by strong third-quarter results and an encouraging earnings outlook. International momentum remains a key strength, with North America showing signs of recovery. In contrast, Coca-Cola’s stock has risen only 2.3% during the same period, highlighting shifting investor sentiment toward PepsiCo’s operational turnaround and margin-improvement efforts.

From a valuation standpoint, PEP currently trades at a lower forward P/E multiple of 17.88X compared to Coca-Cola’s 21.94X, making it more attractively priced. PepsiCo’s diversity, pricing power, and innovation engine make it a compelling long-term holding. While Coca-Cola appears pricey, its valuations reflect its strong brand equity, disciplined capital strategy, and exposure to high-growth regions.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

How Does Zacks Consensus Estimate Compare?

PepsiCo’s EPS estimates for 2025 and 2026 have moved up slightly, with 2025 revenues projected to increase 1.8% year over year to $93.5 billion. However, EPS is expected to decline 0.6% year over year to $8.11.

Image Source: Zacks Investment Research

Coca-Cola’s EPS estimates for 2025 and 2026 have also increased, with 2025 revenues and EPS expected to rise 2.8% and 3.5% year over year, respectively, to $48.4 billion and $2.98 per share.

Image Source: Zacks Investment Research

PEP vs. KO: Who Has the Edge?

In the ultimate face-off between Coca-Cola and PepsiCo, the scale tilts toward PepsiCo due to its stronger near-term performance, attractive valuation, and growth potential. Its diversified portfolio spans beverages and snacks, offering multiple profit engines and resilience against category-specific slowdowns. Recent rallies underscore investor confidence in its revitalized innovation agenda, digital transformation, and operational efficiency.

While Coca-Cola excels in core beverage dominance and brand legacy, it lacks the same breadth of growth drivers that PepsiCo’s multi-category structure provides. PepsiCo’s cheaper valuation relative to its rival amplifies its investment appeal, particularly given its consistent international momentum and robust execution in North America. The recent upward revision in earnings estimates reflects optimism about its capacity to sustain profitability and margin expansion.

PEP currently carries a Zacks Rank #2 (Buy) and KO has a Zacks Rank #3 (Hold).

{kind=link}

Post a Comment for "Coca-Cola vs. PepsiCo: Who Will Reign Supreme?"

Post a Comment