Warner Music Group Targets 150–200 Basis Points Margin Boost by 2026 Amid AI and Growth Momentum

Earnings Call Insights: Warner Music Group Corp. (WMG) Q4 2025

Management View

Robert Kyncl, President, CEO & Director, emphasized the company's progress during the call, stating, "we've improved our market share and delivered profitable growth, all while realigning our company to capitalize on the tremendous set of opportunities we have ahead." He highlighted that in the U.S., market share increased by 0.6 percentage points year-over-year and globally, WMG's share of the Spotify top 200 rose by 6 percentage points compared to fiscal 2024.

Kyncl also mentioned new deals with key DSP partners, explaining, "our new agreements with key DSP partners better reflect music's ever-growing value and provide greater certainty around our economics." He further discussed the company's approach to generative AI, stating, "we've developed a set of principles that will govern how we engage with AI platforms. We will only make agreements with partners who commit to licensed models while securing economic terms that properly reflect the value of music."

Armin Zerza, Executive VP & CFO, noted, "Q4 has been a quarter of acceleration as we delivered record high quarterly revenue as well as our highest year-over-year growth in nearly 2 years." He pointed out a 13% total revenue growth and 64% growth in artist services, crediting "WMX led merch campaigns for Oasis and My Chemical Romance." Zerza added, "we are on track to deliver against our reorganization and related cost savings program of $200 million in annualized savings in 2026, increasing to $300 million in 2027."

Outlook

The company expects strong top line growth in 2026, driven by organic investments, high-impact accretive M&A, and contributions from distribution and direct-to-consumer offerings. Zerza stated, "we expect to see strong top line growth, which we look to bolster through focused organic investments and initiatives in our core music business and high-impact accretive M&A as well as contribution from adjacent areas such as distribution and direct-to-consumer offerings."

WMG is targeting adjusted OIBDA margin improvement of 150 to 200 basis points in 2026, with cost savings increasing sequentially throughout the year. Zerza said, "we are on track to deliver against our reorganization and related cost savings program of $200 million in annualized savings in 2026, increasing to $300 million in 2027."

The company sees "tremendous potential in new incremental growth areas, particularly in AI licensing deals, which we plan to discuss in future calls."

Financial Results

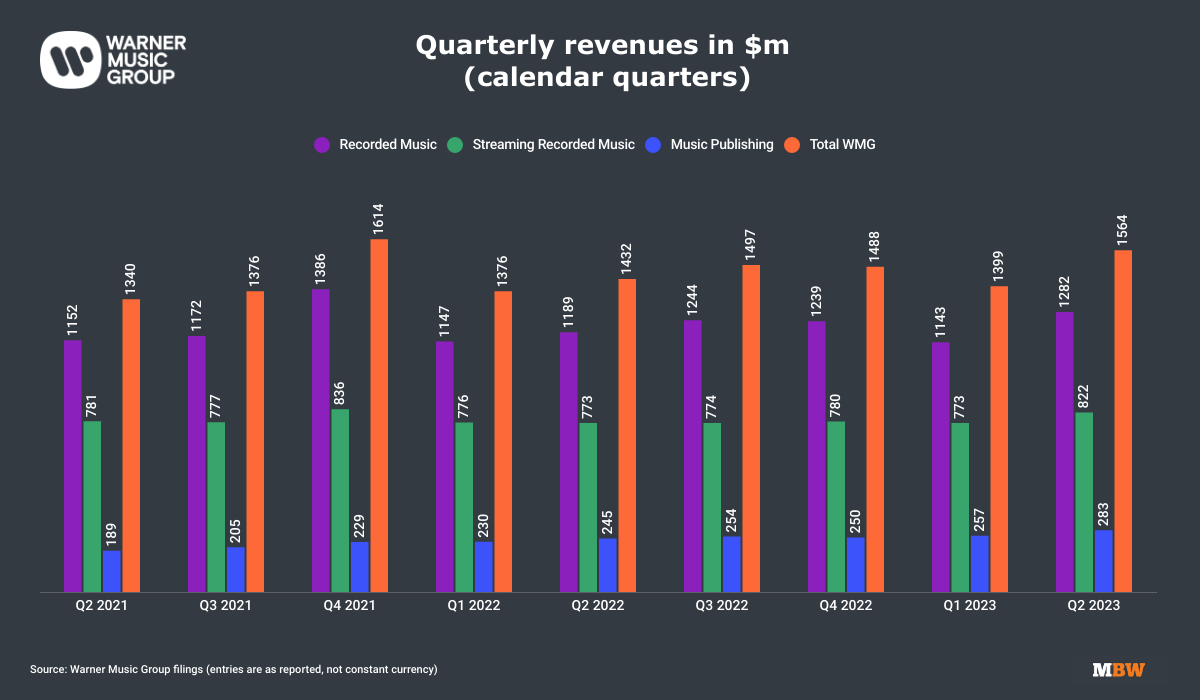

Total revenue grew 13% in Q4 2025, with double-digit growth in Recorded Music and Music Publishing. Recorded Music subscription streaming increased 8.4% and ad-supported streaming grew 3% on an adjusted basis. Artist services revenue rose 64%, attributed to merch campaigns for Oasis and My Chemical Romance. Adjusted OIBDA rose by 12%, but margins declined slightly due to a revenue mix shift towards lower-margin artist service revenue.

As of September 30, cash balance was $532 million, total debt $4.4 billion, and net debt $3.8 billion.

Q&A

Kutgun Maral, Evercore ISI, asked about WMG's role in capturing incremental value from rights monetization amid AI and DSP innovation. Kyncl responded, "we are determined and have decided that we're the drivers, not the passengers of this incremental opportunity" and outlined WMG's principles on AI dealmaking: "We'll do agreements with partners who commit to licensed models. We'll do it on economic terms that properly reflect the value of music ... artists and songwriters have the opportunity and right to opt in for any new songs that implicate their name, image, likeness and voice."

Benjamin Black, Deutsche Bank, inquired about building blocks for 2026 top line growth and margin expansion. Zerza stated, "we will, of course, benefit from the contractual wholesale price increases that we have agreed now with several top DSPs," and reiterated confidence in margin expansion, targeting "mid- to high 20s" margins in the long term.

Peter Supino, Wolfe Research, asked about market share gains and label performance. Kyncl replied, "Our market share hasn't grown just in 1 or 2 places. It's really been broad-based across both our flagship labels as well as all of our regions."

Michael Morris, Guggenheim Securities, asked about M&A and distribution growth. Zerza explained, "we have a very strong pipeline in place, which, as I mentioned, we expect to start to materialize starting in calendar year '26," and highlighted new leadership in distribution as a catalyst for growth.

Ian Moore, Bernstein, questioned the commercial opportunity in AI licensing. Kyncl described the AI environment as "a very energizing moment in the industry" and emphasized WMG's strategy to "get in early, set the terms and define the future for us."

Sentiment Analysis

Analysts focused on monetization opportunities, margin expansion, and the sustainability of market share gains, expressing a neutral to slightly positive tone, with questions seeking clarity on execution and upside but no overt skepticism.

Management maintained a confident tone during prepared remarks and Q&A, using phrases like "we are determined" and "we are confident," while emphasizing proactive strategy and broad-based success.

Compared to the previous quarter, both analysts and management displayed increased confidence, with less focus on organizational tension and more discussion of tangible results and future initiatives.

Quarter-over-Quarter Comparison

Q4 showed a clear acceleration in revenue and market share versus Q3, with revenue growth rising to 13% from 7% in the prior quarter. Management's language shifted from describing strategic plans and organizational changes in Q3 to celebrating broad-based execution and market share gains in Q4.

Analysts in Q4 probed more about execution details and future growth levers, especially in AI and M&A, compared to Q3’s focus on restructuring and cost initiatives. Margin expansion guidance remained consistent, but Q4 featured more specifics on savings timelines and new revenue streams.

Risks and Concerns

The company acknowledged the potential risks of generative AI, emphasizing the need to "protect the rights of our artists and songwriters while simultaneously growing new revenue streams on their behalf." Management highlighted ongoing cost control and efficiency measures as crucial for sustaining margin improvement.

Analysts raised concerns about maintaining market share gains and the balance between cost savings and reinvestment for growth.

Final Takeaway

Warner Music Group closed fiscal 2025 with accelerating revenue growth, improved market share, and a commitment to driving further top and bottom line gains in 2026, underpinned by new DSP deals, proactive engagement with AI platforms, and an ongoing cost savings program targeting $200 million in annualized savings. Management projects strong momentum into 2026, supported by operational streamlining, strategic investments, and a robust pipeline for M&A and new business models.

{kind=link}

Post a Comment for "Warner Music Group Targets 150–200 Basis Points Margin Boost by 2026 Amid AI and Growth Momentum"

Post a Comment