Bros vs. Starbucks: Which Beverage Giant Has More Potential?

Strategic Outlook for Dutch Bros and Starbucks in the Specialty Coffee Market

Dutch Bros Inc. (BROS) and Starbucks Corporation (SBUX) are two major players in the specialty coffee market, each navigating a dynamic landscape shaped by evolving consumer preferences, inflationary pressures, and shifting traffic patterns. As the coffee category stabilizes after a period of volatility, both brands are adopting distinct strategies to drive growth and maintain their competitive edge.

For investors looking to identify which coffee stock offers more upside potential, it's essential to analyze the fundamentals, growth catalysts, and risk profiles of both companies. This evaluation can help determine which brand is better positioned to capitalize on emerging opportunities.

The Case for Dutch Bros

Dutch Bros continues to focus on long-term growth, balancing disciplined unit expansion with enhancements to the customer experience. The company’s strategy centers on accelerating shop development, strengthening digital engagement, and expanding its product offering to reinforce its competitive positioning. With strong unit economics, a robust operator pipeline, and increasing visibility into its multiyear development roadmap, Dutch Bros remains committed to scaling its nationwide footprint without compromising the culture-forward service model at the core of the brand.

A key component of this strategy is the rollout of its hot food program. As of the third quarter of 2025, approximately 160 shops offer food, delivering steady ticket and transaction lifts alongside improving customer and Broista feedback. Early results indicate roughly a 4% comp benefit in participating shops, underscoring food’s potential to complement the company’s beverage-first model by strengthening morning daypart relevance and adding incremental sales opportunity.

As the program scales through 2026, Dutch Bros expects additional operational learnings and product refinement to support broader adoption and sustained performance. At the same time, the company is expanding its digital ecosystem through enhancements in Order Ahead functionality, loyalty segmentation, and mobile user experience. Order Ahead reached a 13% mix in the third quarter of 2025, functioning as a meaningful driver of loyalty enrollment and engagement.

Improvements in pickup-time accuracy, promotional targeting, and analytics capabilities are helping to drive higher frequency and improve guest satisfaction. Dutch Bros is also making progress in cost efficiency and capital discipline, with build-to-suit development lowering average shop CapEx and strengthening return profiles.

However, near-term margin pressures remain a consideration due to higher coffee costs, rising occupancy expenses, and incremental labor headwinds weighing on shop-level profitability. These factors may limit margin expansion in the short term.

The Case for Starbucks

Starbucks continues to face meaningful operational and brand-level challenges that are weighing on its near-term outlook. Despite the launch of its “Back to Starbucks” plan, U.S. traffic has not shown the degree of stabilization management had hoped for, with continued softness across several customer cohorts and weaker afternoon-daypart performance.

While the company has introduced new beverage platforms and promotional activity to reignite demand, the early benefits remain limited relative to the scale of traffic pressures. Execution issues remain a point of concern, with persistent throughput bottlenecks, uneven service consistency, and a need for accelerated in-store process redesigns signaling operational friction.

Efforts to modernize equipment and shift labor deployment are underway, but these initiatives require time, capital, and training before they can translate into measurable improvements in customer experience or sales conversion. Internationally, performance remains mixed, with China experiencing volatile recovery trends due to competitive intensity, cautious consumer spending, and uneven traffic patterns.

Cost pressures further complicate the near-term setup, with wage inflation, elevated input costs, and continued investments in digital infrastructure and store renovations constraining margin recovery. Management has reiterated its commitment to expense discipline and long-term brand-building investments, but the combination of soft traffic, rising costs, and execution risk leaves limited room for near-term upside.

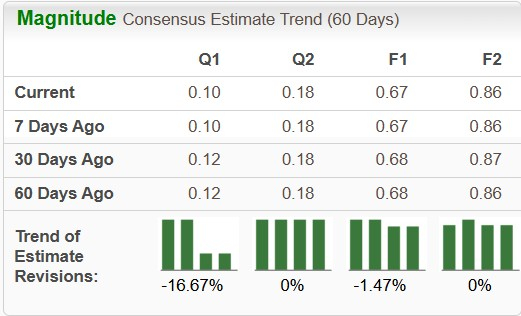

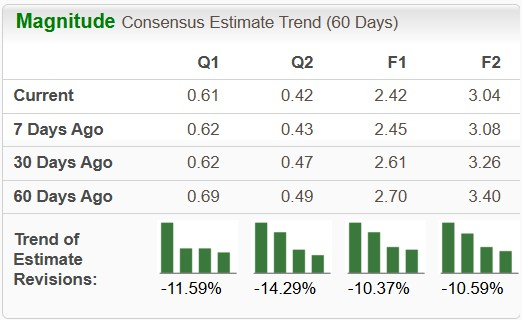

Zacks Consensus Estimates for BROS and SBUX

The Zacks Consensus Estimate for Dutch Bros’ 2026 sales and earnings per share (EPS) suggests year-over-year increases of 24.2% and 27.6%, respectively. In the past 60 days, earnings estimates for 2026 have remained unchanged.

Image Source: Zacks Investment Research

For Starbucks, the Zacks Consensus Estimate for fiscal 2026 sales and EPS suggests year-over-year increases of 3.5% and 13.6%, respectively. In the past 60 days, earnings estimates for fiscal 2026 have declined 10.4% to $2.42.

Image Source: Zacks Investment Research

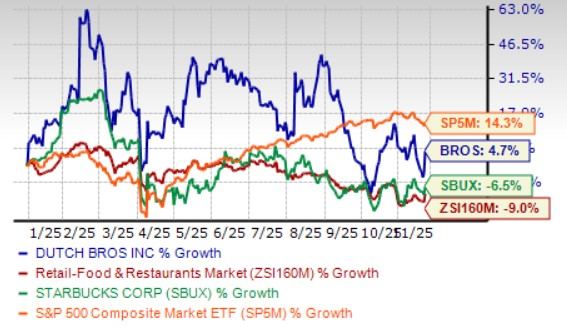

Price Performance and Valuation: BROS vs. SBUX

Dutch Bros’ stock has gained 4.7% so far this year against the industry’s fall of 9%, while the S&P 500 witnessed growth of 14.3%. Meanwhile, SBUX shares have declined 6.5% over the same time.

Image Source: Zacks Investment Research

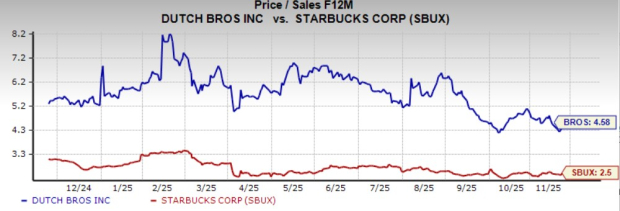

Dutch Bros trades at a forward 12-month price-to-sales (P/S) ratio of 4.58, above the industry average of 3.43 over the last year. In contrast, SBUX commands a lower forward P/S of 2.5.

Image Source: Zacks Investment Research

End Notes

At this juncture, Dutch Bros appears better positioned to deliver consistent growth and operational momentum, supported by accelerating shop development, strengthening digital engagement, and early traction from its expanding food initiative. The Zacks Consensus Estimate trends also favor BROS, reflecting steadier forward expectations relative to Starbucks, whose performance has softened in recent months amid ongoing traffic weakness, operational friction, and slower-than-anticipated international recovery.

Additionally, Dutch Bros has demonstrated comparatively stronger stock performance year to date, underscoring investor confidence in its execution and strategic visibility, even as it trades at a premium multiple. By contrast, Starbucks continues to navigate a more complex turnaround with greater uncertainty around timing and margin recovery. Accordingly, Dutch Bros represents the more compelling pick in the current environment, supported by a clearer growth pathway and more resilient earnings momentum.

Dutch Bros currently carries a Zacks Rank #3 (Hold), while Starbucks has a Zacks Rank #4 (Sell).

{kind=link}

Post a Comment for "Bros vs. Starbucks: Which Beverage Giant Has More Potential?"

Post a Comment